The SSS residential solar financing program is a planned loan facility that will help qualified Social Security System members finance solar panel installations for their homes.

Officially called the Energy Sustainability Loan Program, the initiative is intended to reduce the upfront cost of residential solar and help Filipino families manage rising electricity expenses.

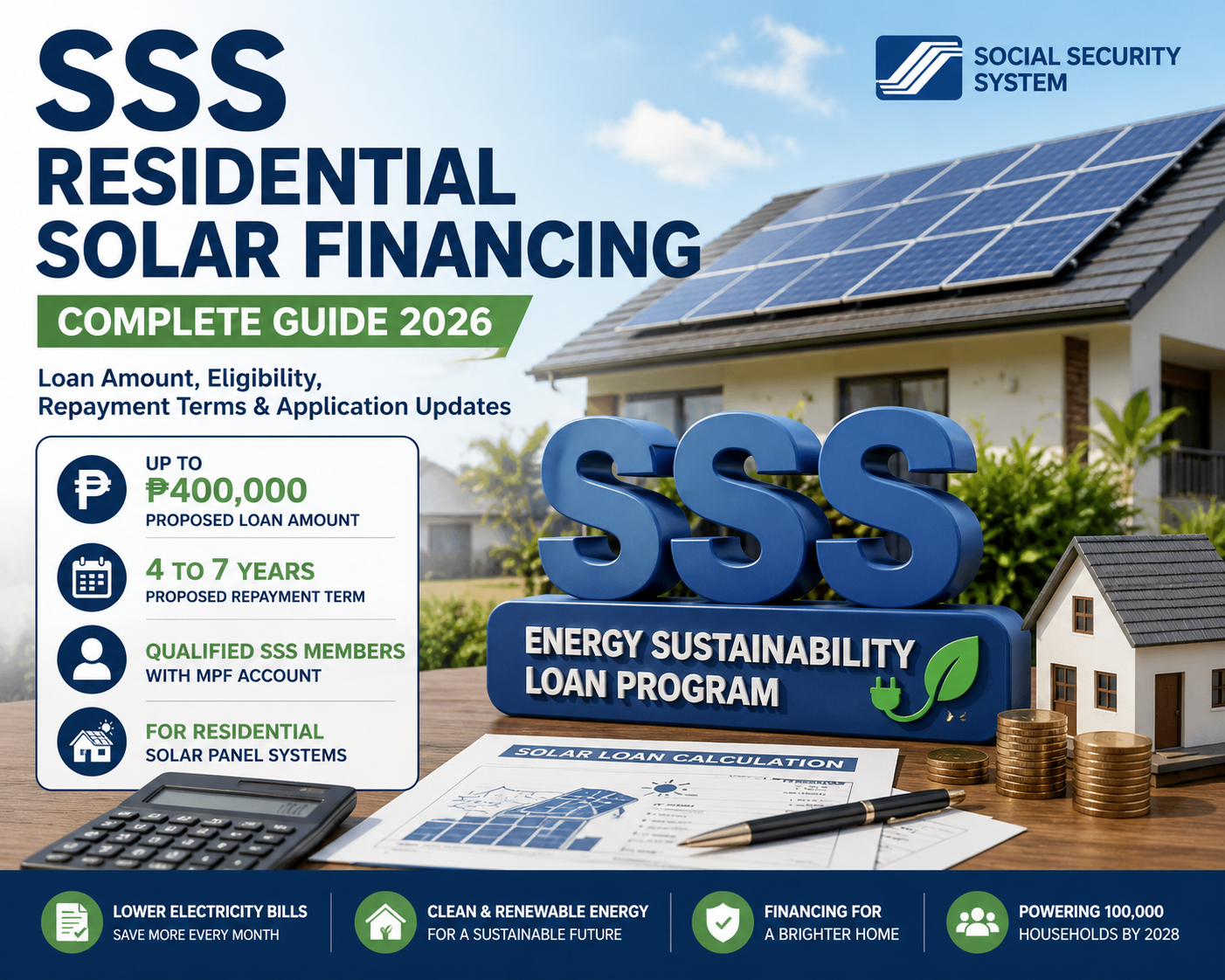

SSS has confirmed that qualified members with a Mandatory Provident Fund account may finance a residential solar panel system with repayment terms of up to seven years. The agency plans to support at least 100,000 households by 2028.

More recent reports indicate that SSS is considering loan amounts between ₱300,000 and ₱400,000, repayable over four to seven years. These figures remain proposed until SSS releases its final circular and implementing guidelines.

Before choosing a system or loan amount, homeowners can use the Solar Loan Payment and Savings Calculator to compare estimated monthly payments, total interest, utility savings, and cash flow.

SSS Residential Solar Financing Quick Facts

| Program detail | Current information |

|---|---|

| Official name | Energy Sustainability Loan Program |

| Intended purpose | Residential solar panel installation |

| Reported maximum loan | Approximately ₱300,000 to ₱400,000 |

| Repayment term | Up to seven years |

| Initial eligible group | Qualified SSS members with a Mandatory Provident Fund account |

| Relevant Monthly Salary Credit | Above ₱20,000 |

| Planned rollout | September 2026 |

| Target beneficiaries | At least 100,000 homes by 2028 |

| Interest rate | Not yet final |

| Application status | Not yet open as of July 14, 2026 |

The official SSS announcement confirms the program purpose, provident-fund eligibility, seven-year maximum repayment period, and September rollout. The reported ₱300,000-to-₱400,000 amount comes from July 2026 statements and must still be confirmed in the final program rules.

Is the SSS Solar Loan Open for Applications?

No. The SSS Energy Sustainability Loan is not yet accepting applications as of July 14, 2026.

SSS announced that it was preparing to roll out the program in September 2026. However, the agency has not yet published a dedicated application page, final circular, official application form, documentary checklist, or list of approved solar installers.

Applicants should wait for an announcement through the official SSS website, My. SSS portal, SSS mobile app, or verified SSS communication channels.

Be cautious of installers or social media accounts claiming they can

- Reserve an SSS solar-loan slot

- Guarantee approval

- Collect an advance application fee

- Submit an application before the official launch

- Sell a system already approved by SSS

- Provide an official SSS application form

No official public application form is currently available.

What Is the SSS Energy Sustainability Loan?

The Energy Sustainability Loan is a proposed financing program specifically intended for residential solar panel installations.

It is designed to help eligible SSS members spread the cost of a home solar system over several years rather than paying the entire installation cost upfront.

The program may help households:

- Lower electricity purchased from the grid

- Reduce exposure to future electricity-price increases

- Finance solar equipment without a large cash payment

- Add renewable energy to their homes

- Improve long-term household energy planning

- Combine solar generation with storage when permitted

SSS describes the program as part of its response to the economic pressures created by high energy costs. It aims to finance installations for at least 100,000 homes by 2028.

How Much Can Members Borrow?

SSS has not yet published a final loan table.

In July 2026, the SSS president said the agency was considering a maximum amount of approximately ₱300,000 to ₱400,000. News reports have therefore commonly described the program as an SSS solar loan of up to ₱400,000.

The amount approved for an individual borrower may eventually depend on:

- Actual solar-system price

- Member’s capacity to repay

- Monthly Salary Credit

- SSS contribution history

- Mandatory Provident Fund balance or status

- Existing SSS loans

- Household income

- Installer quotation

- Property documentation

- Technical suitability of the proposed system

- Final SSS credit rules

The maximum program limit should not be treated as the amount every applicant will receive.

A household that needs a smaller grid-tied system may not need to borrow the full amount. Before requesting quotations, use the Solar System Size Calculator to estimate the array capacity and approximate number of panels required from actual electricity consumption.

Proposed Repayment Period

SSS has officially stated that the residential solar financing may be payable for up to seven years. More recent reports indicate that members may be offered terms ranging from four to seven years.

A longer loan term generally produces a lower monthly payment, but it can increase the total amount of interest paid.

Before selecting a repayment period, compare:

- Monthly amortization

- Total interest over the loan

- Current electricity bill

- Estimated monthly solar savings

- Expected system production

- Equipment warranty

- Maintenance costs

- Inverter replacement risk

- Battery replacement cost, when applicable

- Household income stability

The Solar Loan Payment and Savings Calculator can help compare different loan amounts, rates, and repayment terms.

What Will the Interest Rate Be?

The official SSS solar-loan interest rate has not yet been released.

Recent reporting indicates that the rate may be set slightly above the prevailing Treasury bill rate, but SSS has not confirmed the final percentage, whether it will remain fixed, or how fees will affect the effective borrowing cost.

Applicants should wait for the official program circular to confirm:

- Nominal annual interest rate

- Effective annual interest rate

- Fixed or variable rate

- Processing fee

- Service charge

- Insurance costs

- Late-payment penalties

- Prepayment conditions

- Loan-release deductions

- Total amount payable

A low advertised rate does not always mean the loan is inexpensive. Fees and deductions can increase the real financing cost.

Possible Monthly Payments

The table below is an illustration only. It is not an official SSS amortization schedule.

Illustrative Payments for a ₱300,000 Loan

| Term | Illustrative rate | Approximate monthly payment |

|---|---|---|

| 4 years | 6% | ₱7,045 |

| 5 years | 6% | ₱5,800 |

| 7 years | 6% | ₱4,382 |

| 4 years | 8% | ₱7,324 |

| 5 years | 8% | ₱6,083 |

| 7 years | 8% | ₱4,676 |

Illustrative Payments for a ₱400,000 Loan

| Term | Illustrative rate | Approximate monthly payment |

|---|---|---|

| 4 years | 6% | ₱9,394 |

| 5 years | 6% | ₱7,733 |

| 7 years | 6% | ₱5,843 |

| 4 years | 8% | ₱9,765 |

| 5 years | 8% | ₱8,111 |

| 7 years | 8% | ₱6,235 |

These estimates assume standard monthly amortization with no processing fees, insurance charges, or other deductions. Actual SSS payments may differ.

Use the Solar Loan Payment and Savings Calculator to test your preferred amount, loan term, electricity rate, and estimated solar production.

Who May Qualify for SSS Residential Solar Financing?

The confirmed initial eligibility requirement is that the member must have a Mandatory Provident Fund account.

The Mandatory Provident Fund automatically covers members contributing under the regular SSS program with a monthly salary credit above ₱20,000.

Potential applicants may include the following qualified individuals:

- Private-sector employees

- Self-employed members

- Voluntary members

- Overseas Filipino Workers

- Household employees

- Other covered members who meet the final contribution and provident-fund requirements

SSS has not yet confirmed which membership categories will be included or excluded.

Possible Eligibility Requirements

The final qualifications have not been published. Based on the announced program and common lending requirements, SSS may consider conditions such as the following:

- Active SSS membership

- Mandatory Provident Fund coverage

- Monthly Salary Credit above ₱20,000

- Minimum number of posted contributions

- Recent contribution activity

- No disqualifying overdue SSS loans

- Sufficient repayment capacity

- Active My.SSS account

- Updated contact details

- Approved disbursement account

- Ownership or authorized use of the property

- Residential property located in the Philippines

- Qualified solar installer

- Technically suitable roof or installation area

- Compliance with electrical and utility requirements

These are possible requirements, not a final official checklist.

What Is the Mandatory Provident Fund?

The Mandatory Provident Fund is a compulsory retirement-savings component for covered SSS members with a monthly salary credit above ₱20,000.

It was previously associated with the Workers’ Investment and Savings Program and is now part of the broader MySSS Pension Booster structure.

SSS has specifically identified members with a Mandatory Provident Fund account as the initial eligible group for the Energy Sustainability Loan.

How to Check Your Account

Members can review their records through My. SSS:

- Sign in to the official My.SSS member portal.

- Open the contributions or inquiry section.

- Review the posted Monthly Salary Credit.

- Check for Mandatory Provident Fund or related contribution entries.

- Confirm that recent contributions are complete.

- Update incorrect personal or employment information.

Members should not assume they are eligible solely because their current salary exceeds ₱20,000. The final assessment will depend on posted SSS records and the program’s implementing rules.

Expected Documentary Requirements

SSS has not yet released the official document list. Applicants can prepare likely documents in advance but should not pay for unnecessary certifications until the final requirements are published.

Personal and SSS Documents

Possible requirements may include:

- SSS number

- Active My.SSS account

- Valid government-issued identification

- Updated contact information

- Contribution history

- Mandatory Provident Fund record

- Proof of income

- Recent payslips

- Certificate of employment and compensation

- Income Tax Return

- Business-income documents for self-employed members

- OFW employment documents, when applicable

- SSS-approved disbursement account

Property Documents

Possible property requirements may include:

- Transfer Certificate of Title

- Condominium Certificate of Title

- Tax declaration

- Contract of lease

- Written authorization from the property owner

- Proof of residence

- Recent electricity bills

- Roof photographs

- Property-location information

- Structural or roof assessment

The final rules must clarify whether applicants can install solar on a home owned by a spouse, parent, landlord, or other family member.

Solar Project Documents

Possible technical requirements may include:

- Formal installer quotation

- Itemized bill of materials

- Proposed array size

- Solar-panel brand and model

- Inverter brand and model

- Battery specifications, when included

- Mounting-system details

- Single-line electrical diagram

- Installation scope

- Labor cost

- Equipment warranties

- Installation warranty

- Project schedule

- Installer licenses or accreditation

- Roof and shading assessment

Before accepting a quotation, estimate the roof area required with the Solar Panel Roof Area Calculator.

What Equipment May Be Covered?

SSS has confirmed that the program is intended for residential solar panel systems, but it has not released a detailed list of eligible expenses.

The financing may potentially cover:

- Solar photovoltaic panels

- Grid-tied inverter

- Hybrid inverter

- Mounting structures

- DC isolators

- AC and DC circuit protection

- Solar cables and connectors

- Distribution-board modifications

- Installation labor

- Engineering and design

- Testing and commissioning

- Monitoring equipment

- Permits

- Utility-interconnection work

- Net-metering preparation

- Battery storage, if permitted

Applicants should wait for confirmation before assuming that batteries, roof repairs, full-house rewiring, generator integration, or net-metering fees will be financed.

Will Batteries Be Included?

SSS has not confirmed whether the loan will cover home batteries.

A grid-tied system without a battery is normally less expensive and can reduce electricity purchased from the grid during daylight hours. However, a standard grid-tied inverter generally shuts down during an outage for safety.

A hybrid system with batteries may provide backup power, but it costs more and requires careful sizing.

Before including storage in a quotation, use the Solar Battery Size Calculator to estimate the nominal battery capacity needed for the desired backup duration.

Battery buyers should also consider:

- Usable capacity

- Depth of discharge

- Round-trip efficiency

- Continuous output

- Surge capability

- Cycle warranty

- Calendar warranty

- Replacement cost

- Inverter compatibility

- BMS communication

How to Apply for the SSS Solar Loan

The final application process has not been announced. Once the program opens, applicants will likely need to complete the following stages.

Step 1: Review Your SSS Records

Check:

- Membership status

- Monthly Salary Credit

- Posted contributions

- Mandatory Provident Fund entries

- Existing SSS loans

- Overdue balances

- Contact information

- Disbursement account

Resolve incorrect or missing records before submitting a future application.

Step 2: Read the Official SSS Circular

Confirm the final:

- Application opening date

- Eligibility rules

- Maximum loan amount

- Interest rate

- Repayment terms

- Documentary requirements

- Eligible solar equipment

- Property requirements

- Installer rules

- Application channel

- Loan-release method

Step 3: Review Your Electricity Consumption

Collect at least 12 months of electricity bills when possible.

Record:

- Monthly kWh consumption

- Monthly bill amount

- Daytime consumption

- Seasonal changes

- Planned appliances

- Air-conditioning use

- Electric-vehicle plans

- Water-pump use

- Future household expansion

System size should be based on energy consumption, not only the available loan amount.

Step 4: Obtain a Solar Site Assessment

A competent installer should evaluate the following:

- Roof condition

- Roof orientation

- Shading

- Available roof area

- Electrical service

- Main distribution board

- Earthing system

- Desired backup loads

- Utility interconnection

- Safe equipment location

Homes adding a large inverter, battery, or backup-load panel may need a more detailed electrical assessment. Review the Home Electrical Load Calculation and Service Upgrade Guide before approving major electrical changes.

Step 5: Request Itemized Quotations

Obtain quotations from more than one installer.

Every quotation should identify:

- System capacity in kW

- Number and wattage of panels

- Panel manufacturer and model

- Inverter manufacturer and model

- Battery capacity and model, when applicable

- Mounting materials

- Protection devices

- Wiring

- Labor

- Taxes

- Permit costs

- Net-metering services

- Product warranties

- Installation warranty

- Total installed price

Avoid one-line quotations that provide only a total cost.

Step 6: Compare Financial Performance

Use the solar payback calculator to estimate:

- First-year savings

- Simple payback period

- Ten-year net benefit

- Effect of export compensation

- Effect of maintenance expenses

Then compare the projected savings with the proposed monthly loan payment.

Step 7: Submit Through the Official Channel

SSS may eventually accept applications through the following:

- My.SSS portal

- SSS mobile application

- Selected SSS branches

- Approved partner institutions

- Accredited project providers

Do not use a third-party application form unless SSS officially authorizes it.

Step 8: Wait for Approval Before Installation

Do not assume that a system installed before approval will qualify for reimbursement.

The final guidelines may require:

- Prior loan approval

- Approved installer

- Approved quotation

- Direct payment to the supplier

- Inspection before fund release

- Inspection after installation

How to Choose the Correct Solar System

The largest affordable system is not always the best system.

The appropriate design depends on:

- Annual electricity consumption

- Daytime load

- Roof size

- Shading

- Orientation

- Electricity rate

- Export compensation

- Net-metering availability

- Outage frequency

- Desired backup time

- Battery budget

- Future loads

Grid-Tied Solar

Best suited to households primarily seeking bill reduction.

Advantages:

- Lower initial cost

- Fewer components

- Strong daytime savings

- Easier maintenance

Limitation:

- Usually no backup power during a grid outage

Hybrid Solar

Combines solar with batteries and backup functionality.

Advantages:

- Backup power

- Greater self-consumption

- Flexible charging and load control

Limitations:

- Higher cost

- More complex installation

- Battery replacement expense

- Additional compatibility requirements

Off-Grid Solar

Designed for properties without reliable utility power.

Advantages:

- Greater grid independence

- Useful in remote locations

Limitations:

- Larger battery requirement

- More conservative system sizing

- Higher cost

- May require generator support

Households coordinating solar, batteries, smart loads, EV charging, and backup systems should review the Integrated Home Energy Management Guide.

How to Decide Whether the Loan Is Worth It

The solar loan may make financial sense when:

- The system price is competitive

- The interest rate is reasonable

- The roof has good solar access

- The household has significant daytime consumption

- The equipment has reliable warranties

- Monthly savings offset a meaningful share of the payment

- The homeowner expects to remain in the property

- The installer provides dependable after-sales service

It may be less attractive when:

- The roof is heavily shaded

- The installation is overpriced

- The household uses little electricity

- Most production will be exported at a low rate

- The loan contains high fees

- Major roof repairs will soon be required

- The borrower cannot comfortably afford the payment

- The installer cannot provide technical documents

- The proposed production estimate is unrealistic

Calculate at least three scenarios:

- Conservative solar production

- Expected solar production

- Optimistic solar production

The project should remain affordable under the conservative scenario.

Questions to Ask a Solar Installer

Before signing a quotation, ask:

- What is the exact system capacity in kW?

- What annual production is expected?

- Which assumptions were used?

- How much shading was included?

- What percentage of production will be self-consumed?

- What will happen during a power outage?

- Are batteries included?

- Are all protection devices included?

- Who handles permits and net metering?

- What is the panel warranty?

- What is the inverter warranty?

- What is the installation warranty?

- Who provides after-sales service?

- Are monitoring and commissioning included?

- Are there additional costs not shown in the quotation?

Common Solar Financing Mistakes

Borrowing the Maximum Without Proper Sizing

The loan ceiling should not determine the array size. Household consumption and site conditions should determine it.

Comparing the Payment Only With the Current Bill

A loan payment may continue even when production temporarily falls because of weather, faults, maintenance, or equipment failure.

Ignoring Interest and Fees

Compare the total amount payable, not only the monthly amortization.

Assuming Solar Automatically Provides Backup

Standard grid-tied solar usually shuts down during a utility outage.

Buying an Oversized Battery

An unnecessarily large battery increases the project cost and can weaken financial returns.

Accepting Unverified Production Claims

Request the assumptions behind every estimate, including peak sun hours, losses, shading, degradation, and export percentage.

Paying Before Official SSS Approval

Do not make a nonrefundable payment based on the expectation that SSS will approve the project.

Frequently Asked Questions

What is SSS residential solar financing?

It is a planned SSS loan program that will allow qualified members to finance residential solar panel installations.

What is the official program name?

The official announced name is the Energy Sustainability Loan Program.

Is the SSS solar loan open now?

No. Applications are not yet open as of July 14, 2026. SSS announced a planned September rollout but has not released the final application procedure.

How much can I borrow?

SSS has reportedly been considering loans of approximately ₱300,000 to ₱400,000. The final maximum remains subject to the official circular.

How long will repayment take?

SSS has confirmed repayment terms of up to seven years. Recent statements indicate possible terms ranging from four to seven years.

What is the interest rate?

The final interest rate has not been announced.

Who may qualify?

Initial eligibility is expected to include qualified SSS members with a Mandatory Provident Fund account. This fund automatically covers members contributing a monthly salary credit above ₱20,000.

Can voluntary members apply?

The final membership-category rules have not been published.

Can self-employed members apply?

SSS has not yet confirmed the final eligibility rules for self-employed applicants.

Can OFWs apply?

The official announcement does not yet specify whether qualified OFWs will be included.

Will the loan cover batteries?

SSS has not released the final list of eligible components, so battery coverage remains unconfirmed.

Will SSS provide the solar panels?

The program is described as financing for residential solar installations. SSS has not yet explained whether borrowers will select an accredited installer, receive funds directly, or have payments released to a supplier.

Does SSS have approved solar installers?

No official list has been published.

Can I install solar now and apply for reimbursement later?

There is no confirmation that systems installed before loan approval will be eligible. Wait for the official rules before making a financing-dependent purchase.

Where will applications be submitted?

SSS has not announced the final application channel. It may use mine. SSS, its mobile app, branches, or authorized partners.

Is there an application fee?

No official fee schedule has been released. Do not pay anyone for guaranteed approval or an advance reservation.

Final Advice

The SSS residential solar financing program may become an important financing option for Filipino homeowners who want to reduce electricity costs without paying the entire solar-system price upfront.

SSS has confirmed that the program will serve qualified members with a Mandatory Provident Fund account, provide repayment terms of up to seven years, and target at least 100,000 residential installations by 2028.

The reported maximum amount of ₱300,000 to ₱400,000, final interest rate, eligible equipment, documentary requirements, and application process still require official confirmation.

Before applying:

- Update your My. SSS records

- Review your contributions and existing loans

- Collect 12 months of electricity bills

- Calculate the appropriate solar-system size

- Obtain multiple itemized quotations

- Compare monthly payments with realistic savings

- Confirm roof and electrical suitability

- Wait for the official SSS circular

Explore all Home Energy Desk solar calculators to estimate system size, roof area, production, battery capacity, financing cost, exports, and payback before choosing a residential solar system.